Participate in Compass’ Q2-Q3 2014 financial benchmarking study (click here) and inform your financial planning and resource allocation decisions.

Join the free Proformative

For decades, organizations of all sizes and from all kinds of industries have curated and perfected

Look at companies large and small, and everywhere in the world, and you will find that performance management practices these days are remarkably alike, almost everywhere. That bundle of management practices was popularized between the 1950s and the 1980s, starting with the idea of Management by Objectives, proposed by Peter Drucker in his 1954 book, and into the late 1970s, when Michael Porter elevated the idea of competitive advantage, or strategy, to a quasi-science. Since then, “fixed performance contracts” have become almost omnipresent and are until this day considered the standard for managing performance, and for controlling businesses and people.

Starting with the Beyond Budgeting movement in the late 1990s, some have started to question the idea of the static performance contract: the philosophy of budgeting and setting fixed targets in advance, and then measuring and judging actual performance against those pre-defined objectives. Fixed performance contracts, the critics say, are not only inefficient today. They can only be counter-productive in times when uncertainty and surprise become the norm, and when value-creation becomes more complex, instead of remaining just complicated.

The side effects of “fixed performance contracts” are wide-ranging and dramatic. They range from internal stakeholders gaming performance systems and controls (in reaction to target-setting and bonus compensation), to external stakeholders and CFOs rigging the financial markets (in reaction to earnings guidance and expectation management).

Performance Management: Are we riding a dead horse?

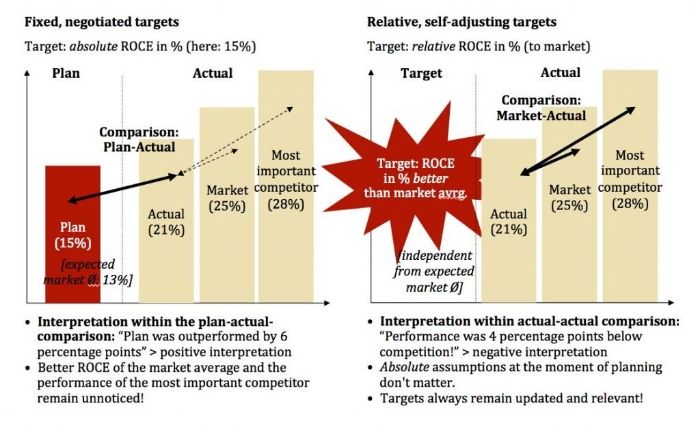

In other words: The performance management practices from the past are broken, and we know it. Uncertainty and complexity have long invalidated planning, forecasting, fixed targets, plan-actual reporting (see Figure 1), and bonus systems. We have outsourced control to markets a long time ago. But instead of letting go of all practices that assume stable, slow-moving, and indeed dull markets, we have continued to optimize and perfect these practices. We have tried to improve a way of managing that has long been straight jackets, or “dead horses.” The very same Peter Drucker once wrote that “90% of what we call management today actually consists of practices that make it hard for people to do their work.” Today, the challenge for us is not just to recognize that, and its consequences. It is to get off the dead horse.

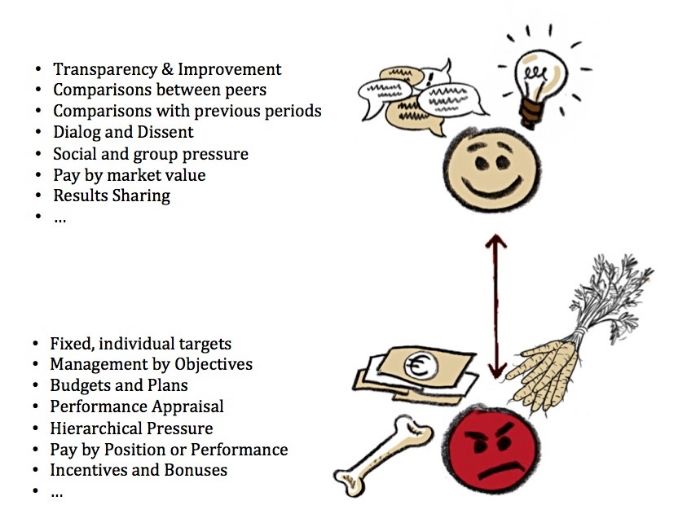

In dynamic markets and value creation, absolute targets weaken control and create misleading incentives (left), while relative measurement enables transparency and adaptive control rooted in self-organization principles (right).

Figure 1: How we fool ourselves, using fixed performance contracts:

Example of a financial performance indicator

The good news is that the solution, or the alternative to fixed performance contracts, has already been around for quite a while, albeit in a relatively small number of startlingly successful “pioneering” organizations. Even though they may seem new and indeed counter-intuitive to many companies and managers today that have been used to the notion of controlling through fixed performance contacts, some larger companies have used relative performance contracts, exclusively, for a few decades. As we learned during the case study research journey of the Beyond Budgeting Round Table (of which I was a director for a few years) that started in 1998, there is a whole world beyond budgeting, fixed targets, incentives and variance reporting. We began labeling this alternative “relative performance contracts” in the early 2000s.

Relative performance contracts are based on the assumption that it is unwise to set fixed targets for managers and teams and then to control their behavior and activities in terms of these targets. The implicit agreement is that management's task is to provide a challenging and open work climate within which employee teams agree to aim for continuous performance improvements: managers and employees must use their knowledge and their own common sense to adapt to changing conditions and environments.

Towards the emerging "relative" performance contracts:

Under this performance contract, decisions are not made at the top. Instead, they are distributed, decentralized, and devolved as far out as possible. This type of performance contract increases, not erodes, mutual trust. Increased transparency and higher expectations (compared to competitors or their equivalent) provide a permanent challenge, which either has to be matched to or whose failure will lead to equally transparent consequences. Responsibility for performance and decision-making are gradually shifted away from the center of the organization towards the periphery. Decentralization thus is key to relative performance contracts.

Figure 2: How to move from fixed to relative performance contacts

Variations of this kind of relative measurement have been used by a few larger companies for decades. An example: In 1971, after severe internal crisis, Swedish bank Handelsbanken began to transform its organizational units into self-managed profit centers with clearly defined customer relationships and highly devolved responsibility for the results. Budgets, fixed targets, quotas, incentives and bonus systems, and indeed also the org chart, and central departments like

To monitor performance, Handelsbanken developed a compellingly simple control system within which teams work on the basis of relative performance measurement based on “real world,” not planned, performance data. Success is no longer measured according to negotiated, planned data, but relative improvement as measured using a limited number of key figures. To do this, the bank as a whole compares itself with its closest rivals. Similarly, regional banks assess their performance monthly and in comparison with other regions, and branches are compared with other branches. All targets, performance assessments and reporting systems are thus based on internal or external competition and continuous improvement.

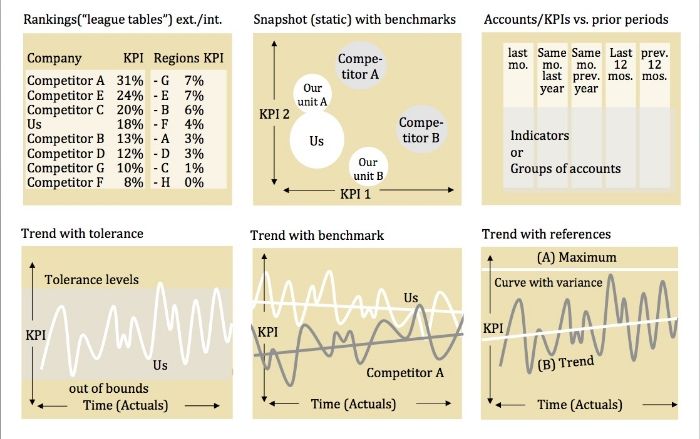

Figure 3: Ways of measuring, without actual-plan-variances, fixed targets, or plans

This 3-layer continuous ranking system has proved to be highly self-regulating and has required only minor modifications over the course of decades. It does not depend on any annual adjustment, hierarchically integrated planning, or internal negotiation. At the same time, it has dramatically increased internal transparency and responsibility of teams to act as if “the branch is the bank.” Employees are driven not by individual targets or group incentives; rather, the system appeals to employees' need to be valued and recognized for their role in helping the organization succeed.

Other larger, successful companies such as Southwest Airlines, Toyota, W.L. Gore, Guardian Industries, Aldi, dm-drogerie markt, or Egon Zehnder International have developed models similar to the Handelsbanken approach. There are enough examples of pioneering companies to give us the courage to overcome traditional thinking and ways of dealing with performance, Now that competitive benchmark date is becoming widely available, and to organizations of all kinds and sizes, at much lower cost than ever before, we have ever more reasons to search for new ways to measure and improve performance more effectively: using real data, not invented numbers.

Niels Pflaeging is an