Very soon, most Proformative readers will be neck-deep in developing next year’s budget. Perhaps now is a good time to think about the pain imposed on business managers by convoluted budgeting. Think too about what you’re asking your finance staff to endure.

Sure, many factors can be blamed for the inevitable disputes. There may be ridiculous growth targets tied to some evangelist’s notion of the company’s ideal value. There may be CEO pet projects that add bloat to the

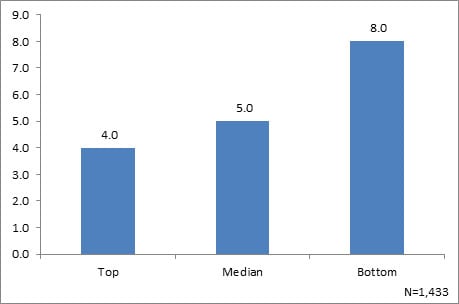

Is your budgeting regime currently reasonable? One metric from APQC's Open Standards Benchmarking® repository offers a way to test for a symptom: the number of budget iterations before final approval (see chart).

The top performers, those in the top quartile, are finished after four or fewer go-arounds. The bottom 25 percent of our study set suffers through twice as many (or much worse) before wrapping things up.

Number of Budget Iterations Produced before Final Approval

You won’t have enough time before budget season dawns to launch an effective overhaul of the budgeting approach. But it could be a smart move to keep an eye open as you along for what should be fixed. When the 2017 budget is finalized and delivered, figure out the sequence of remedial steps you can take to change things up for next year.

Set up a worksheet that has three columns displayed across the top: Stop, Start, or Continue. Perhaps ask your staff to do the same. As you soldier through this year’s exercise, assign budgeting tasks or rules to the category that feels right: Stop, Start or Continue. When all the hub-bub is over, convene your colleagues for a few brainstorming sessions. As a group gain consensus on the most egregious tasks, dumb do-overs, or data mash-ups that can be slated for change.

You can also ask an industrious staffer to start searching for and collecting articles that highlight best practices in budgeting and planning. Goodness knows, there are plenty publicly available. Just steer clear of philosophical debates about the folly of using the annual budget as your primary performance management tool. You already know that’s a silly thing to do.